source: Bloomberg https://www.bloomberg.com/markets, MSCI https://www.msci.com/end-of-day-data-search and ARG Inc.analysis

Equity markets were a mixed bag. We saw a blend of positive and negative news; both locally and internationally. Inflation and measures being taken in an attempt to control it continue to be the primary driver of markets.

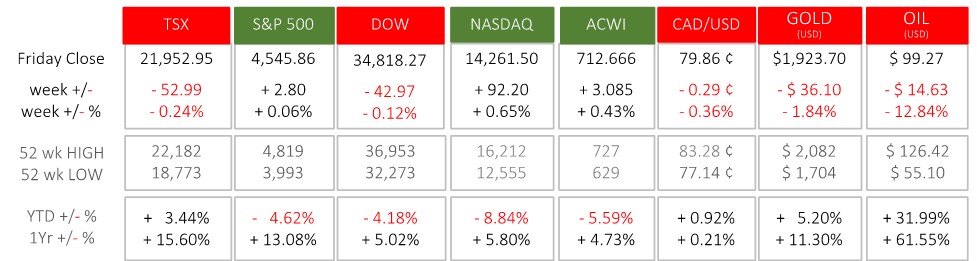

- The price of oil fell last week but is up 32% this year and 62% from one year ago. Higher energy prices will filter through the economy and add to already rapid price increases.

- Central banks anticipate rising inflation and will raise short term interest rates.

- Canadian Gross Domestic Product has rebounded in February with 0.8% growth following January’s Omicron-induced results of 0.2%. The strengthening economy coupled with jobs growth (report scheduled for Friday), and rapidly rising prices that are expected to continue to rise, forces the Bank of Canada to trim back economic growth with higher interest rates at their next meeting in mid-April. StatsCan https://www.cbc.ca/news/business/interest-rate-analysis-1.6402439

- The same economic situation exists in the U.S. (rising inflation, strong employment, GDP growth) except the next meeting of the Federal Reserve’s Open Market Committee is scheduled for early May. President Biden has taken the unusual step to release 1 million barrels of oil daily for the next six months from strategic reserves. This indicated the government is willing to use many inflation-fighting strategies.

- Regarding the geopolitical situation in Ukraine: disruption of energy shipments to western Europe, the rising cost of manufacturing inputs like electricity generated from natural gas, fiscal pressures for governments to increase military spending, and support for refugees will affect markets around the world.

What’s Ahead for this Week and Beyond?

In Canada, February’s building permits and merchandise trade balance will be announced prior to the federal budget on Thursday at 4 pm Eastern. On Friday, the February jobs report will be released.

In the U.S., factory orders, goods and services trade deficit, consumer credit and wholesale inventories for February, and Purchasing Managers Indexes from ISM and Markit for March will be released.